Timing Layered Adjustments Through Pulse Analysis in Depth Markets on Racing and Football Exchanges

Market participants on betting exchanges monitor depth layers in racing and football markets to detect pulse shifts that signal opportunities for position adjustments, and these shifts arise from changes in order flow volume and liquidity distribution. Data from exchange platforms indicates that depth pools in horse racing often exhibit rapid contractions during pre-race periods, while soccer markets display similar patterns around key match events such as substitutions or set pieces. Observers note that combining volume data with price ladder movements allows traders to identify entry and exit points without relying on surface-level odds alone.

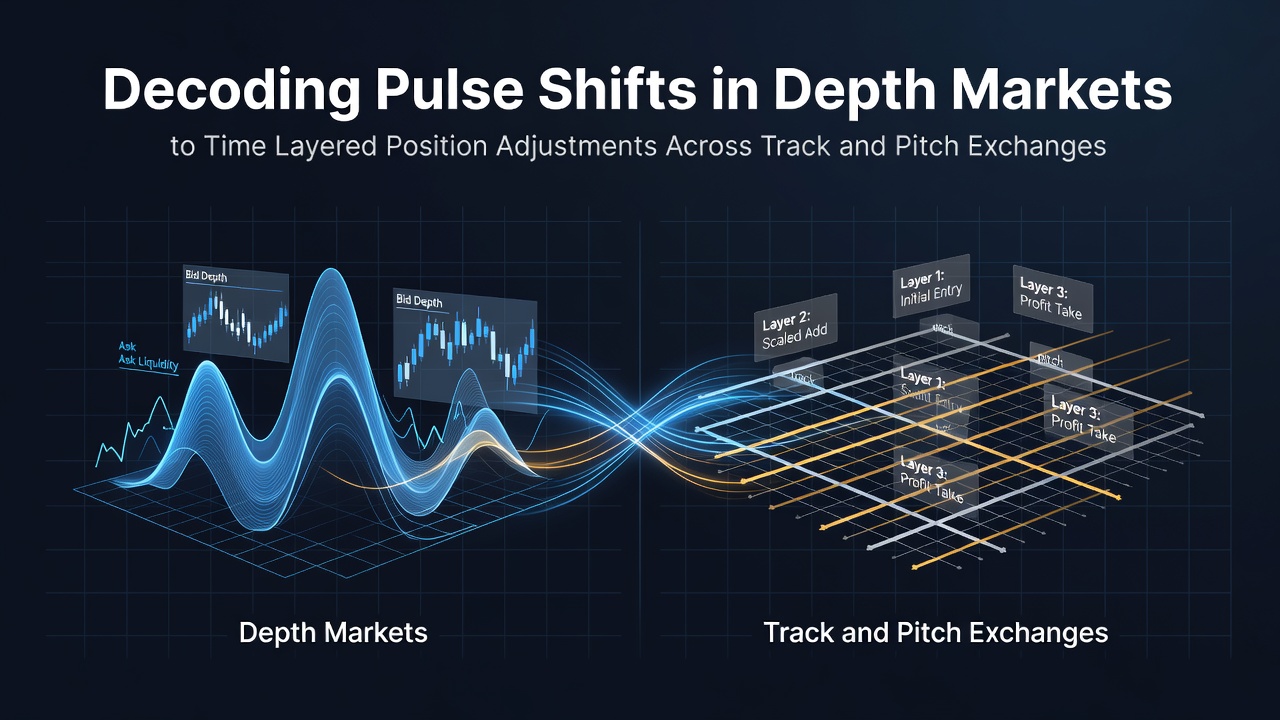

Market Depth Structures Across Track and Pitch Platforms

Depth markets on exchanges consist of stacked back and lay orders at multiple price increments, and analysts track these layers to map liquidity availability in both racing and soccer contracts. Research from the European Gaming and Betting Association shows that racing markets typically maintain thinner depth beyond the top three price points compared with football markets, where in-play liquidity can extend across wider spreads during high-attention periods. Those who study these structures find that pulse shifts occur when large unmatched orders suddenly appear or withdraw, creating temporary imbalances that precede price movements.

June 2026 figures from multiple exchange operators revealed consistent patterns in which depth contractions preceded major odds adjustments in both Premier League fixtures and major racing festivals. Experts have observed that participants who monitor cumulative volume at each layer gain earlier signals than those focused solely on matched trades, and this approach applies equally to turf events and pitch-based contests.

Detecting Pulse Shifts Through Order Flow Indicators

Pulse shifts manifest as abrupt changes in the rate of order placement and cancellation within specific depth layers, and software tools aggregate this data to highlight acceleration points. Studies on market microstructure indicate that a surge in lay orders at a particular price level often precedes a back-price retreat in racing markets, while soccer depth pools show analogous behavior around goal-scoring windows. People who examine tick-by-tick records note that these pulses frequently cluster before scheduled events such as race starts or halftime intervals.

Volume cluster analysis provides additional context, because isolated spikes without corresponding price movement suggest latent interest that may trigger later adjustments. Data indicates that repeated pulses at the same depth level strengthen the reliability of subsequent position timing decisions across both track and pitch exchanges.

Executing Layered Position Adjustments

Traders adjust positions by scaling into or out of back-lay combinations once a pulse shift registers across multiple depth layers, and this method requires simultaneous monitoring of matched volume and unmatched order stacks. Case records from exchange activity demonstrate that layered entries reduce slippage compared with single-price executions, particularly when liquidity thins during evening racing cards or late-stage soccer matches. Those who apply this technique often stagger adjustments across adjacent price increments to maintain exposure while responding to shifting depth.

Timing relies on confirmation signals such as sustained volume increases at the next depth level, and platforms supply historical pulse data that participants reference for pattern recognition. June 2026 records show elevated adjustment frequency during overlapping racing and football schedules, when cross-market liquidity flows created additional pulse opportunities in depth pools.

Comparative Patterns in Racing and Soccer Depth Pools

Racing markets tend to produce shorter-duration pulses tied to betting windows before each race, whereas soccer depth exhibits longer sequences linked to match narrative developments. According to analysis from the Responsible Gambling Council of Canada, both asset classes display measurable correlations between depth contraction speed and subsequent price volatility. Observers note that horse racing pulses often resolve within minutes of detection, while football pulses can persist through extended in-play phases.

Market participants who track both environments simultaneously identify instances where a pulse in one asset class influences liquidity in the other, particularly when major events coincide on the same calendar day. This cross-asset dynamic appeared frequently in June 2026 data sets compiled by exchange analytics providers.

Conclusion

Decoding pulse shifts supplies exchange users with measurable signals for timing layered position adjustments in racing and football depth markets, and continued data collection supports refinement of these techniques. Figures from June 2026 confirm that depth monitoring delivers consistent indicators across both track and pitch platforms when applied systematically. Participants who integrate volume cluster tracking with order flow analysis maintain structured approaches to position management amid fluctuating liquidity conditions.