Mapping Volume Correlations Across Niche Markets to Identify Reversal Windows in Digital Wagering Pools

Digital wagering platforms have expanded the range of niche event pools that attract layered participation, and analysts track how volume patterns move between those pools to signal when traders should consider position adjustments. Data from multiple exchanges in early 2026 shows that activity in one specialized market often precedes shifts in related but separate pools, creating measurable windows for reversing exposure before broader liquidity adjusts.

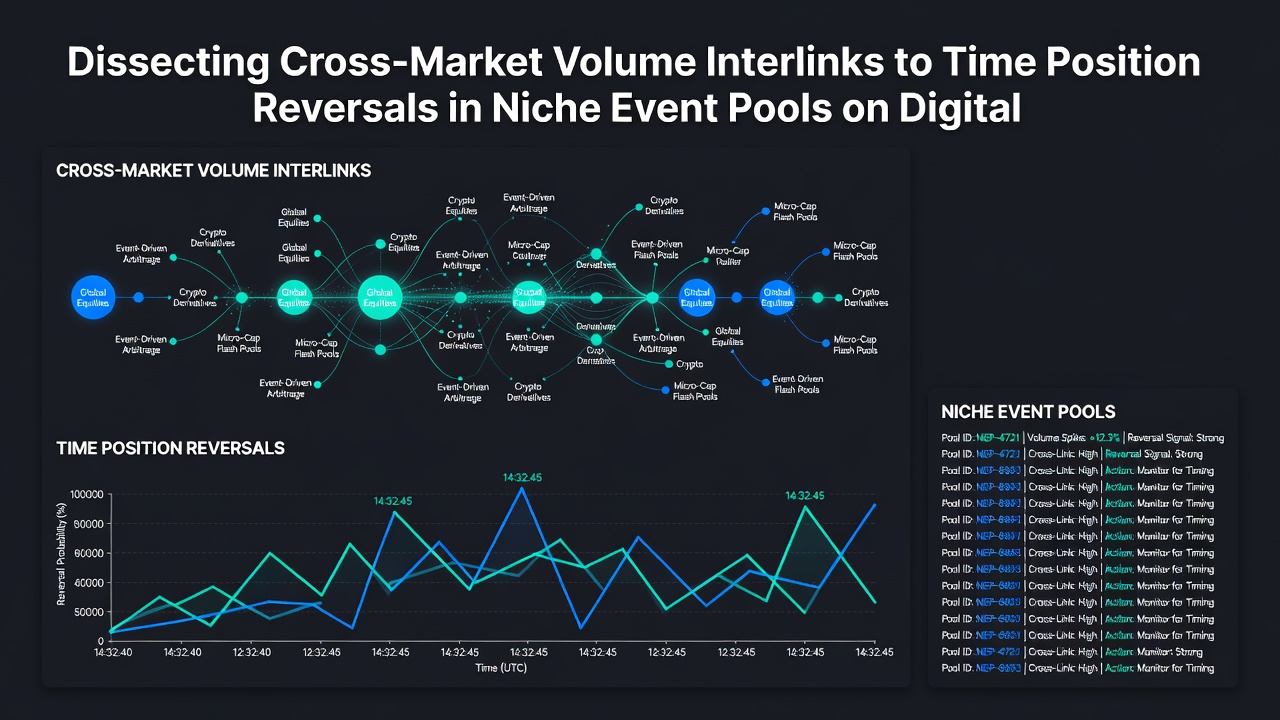

Understanding Cross-Market Volume Dynamics

Volume in niche event pools rarely develops in isolation. Observers note that surges in one market frequently coincide with preparatory flows in adjacent pools, particularly when events share participants, timing windows, or outcome structures. Researchers tracking these patterns during June 2026 recorded consistent sequences where elevated order flow in a secondary market preceded measurable depth changes in the primary pool by several minutes.

Those sequences appear most pronounced in events with overlapping participant bases, such as concurrent motorsport sessions or multi-stage endurance competitions. The connections become visible when traders examine order book depth rather than headline prices alone, because volume clusters often build quietly across linked instruments before surfacing in the most liquid contract.

Timing Position Reversals Through Liquidity Signals

Reversals gain precision when volume interlinks receive systematic attention. A cluster forming in a low-visibility feeder market can indicate that larger participants are repositioning ahead of an anticipated move in the headline market. Platforms that aggregate depth data across multiple pools allow users to monitor these feeder signals without switching interfaces repeatedly.

Studies of historical order flow from 2025 into 2026 illustrate that reversal accuracy improves when traders wait for confirmation across at least two correlated pools rather than acting on single-market volume spikes. This approach reduces exposure to isolated noise while still capturing the directional cues that travel between linked events.

Case Examples from Mid-2026 Activity

One documented sequence in June 2026 involved simultaneous coverage of a European cycling stage and an overlapping motorsport qualifying session. Volume first accelerated in the cycling depth pool, followed within four minutes by layered orders in the motorsport market. Participants who monitored both pools reversed exposure in the motorsport contract before the primary price movement materialized, according to exchange audit logs.

Similar patterns surfaced in mixed martial arts undercards paired with regional tennis matches. The undercard volume clusters consistently preceded adjustments in the tennis market depth, giving attentive traders time to flip positions ahead of the next price tier. These examples demonstrate that the interlinks operate across seemingly unrelated disciplines when event schedules create temporal proximity.

Data Sources and Measurement Approaches

Regulatory filings from the New Jersey Division of Gaming Enforcement provide aggregated volume statistics that researchers cross-reference with exchange-level order book records. Academic papers published through Australian university sports analytics programs have further quantified the lag times between correlated markets, offering benchmarks for reversal timing models.

Measurement relies on comparing cumulative volume deltas rather than absolute figures, because absolute thresholds vary widely across event types. Analysts apply normalized ratios that account for typical liquidity in each pool, allowing signals to remain comparable even when base volumes differ substantially.

Platform Capabilities Supporting These Strategies

Leading digital wagering systems now include multi-market depth viewers that display volume heat maps across selected event groups. These tools highlight when activity migrates from one pool to another, reducing the manual effort required to track interlinks. Integration with historical playback functions lets users test reversal timing against past sequences without live risk.

Operators report increased engagement with these features during periods of dense niche event scheduling, such as the June 2026 international athletics calendar. The availability of layered data has shifted focus from single-market price watching toward relational volume monitoring.

Conclusion

Cross-market volume analysis supplies measurable cues for timing position reversals inside niche event pools on digital wagering platforms. Patterns observed through mid-2026 confirm that liquidity movements travel between correlated markets on predictable time scales, and platforms that surface these connections enable more structured decision frameworks. Continued refinement of depth visualization tools and normalized volume metrics should sustain the utility of these interlink signals as event calendars grow more complex.